The long-running premiumisation trend in beverage alcohol weakened significantly in the first half of 2023, as consumers felt the full impact of economic pressures and geopolitical uncertainty.

Key trends fuelling the deceleration included the slowing of premium-and-above agave expansion in the US, losses across the wine category – including Champagne – and softer growth for high-end beer in markets such as Brazil and Spain.

Nevertheless, pockets of premiumisation endure in Asia in particular, with high-end baijiu performing well in China, and markets such as India, the Philippines and Thailand recording dynamic growth in high-end spirits consumption. Meanwhile, beer was boosted by the reopening on-premise in China and trading up in the UK, US and Mexico.

Premium+ volumes grow at a slower rate

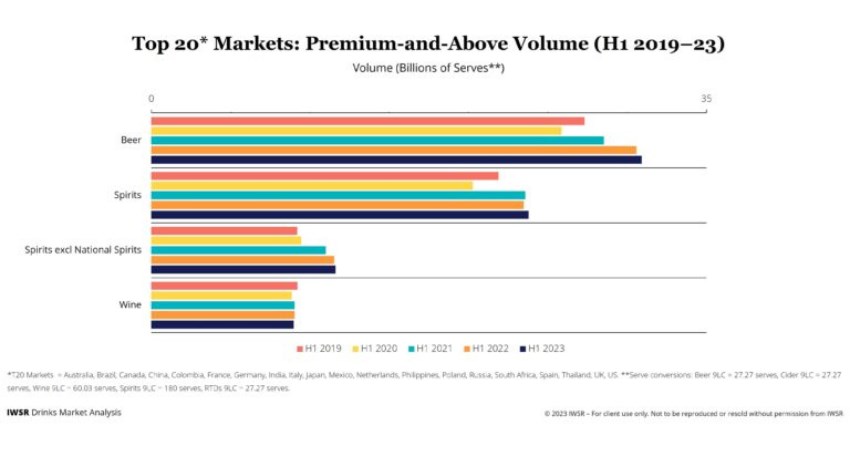

Across 20 key markets (that make up over 75% of total global volumes), total beverage alcohol premium-plus volume consumption in the first half of 2023 was 11% higher than for the same period in 2019; however, this growth rate is slowing, with volumes only increasing by 1% between H1 2022 and 2023. A similar trend of slowing growth is evident across premium+ volumes for total beer and spirits as well (see chart below).

“The growth rate of premium-and-above products weakened significantly across beer and spirits during the first half of 2023, although their share of overall category volumes broadly continued to increase,” notes Emily Neill, COO research, IWSR.

“Economic pressures did not relent, as inflation remained high – a backdrop that was more globally widespread than during the same period last year. Geopolitical uncertainty from the war in Ukraine heightened the pressures mounting on brand owners, which passed on increased costs to consumers.”

Click HERE to read the full article.